When it comes to protecting your health and spending your money wisely, do you really know what kind of plans is best for you and your family? Today, we will explain the difference between a traditional health insurance and an indemnity plan.

differences between health insurance (major coverage) & indemnity plan?

Choosing a health insurance plan in the USA is always a tedious task. Although the terms and vocabulary are barbaric it is essential to understand them and especially to understand the limits offered by your plan.

Do not think that an indemnity plan does replace your primary coverage. It is only a supplement.

What is an Indemnity Plan?

Indemnity plans provide limited benefits. An indemnity plan is a supplement to your health insurance (major medical coverage) and is not a substitute for the minimum essential coverage required by the affordable care act (ACA). According to the conditions of the contract, your indemnity plan guarantees you a certain level of benefit by covering a part of your Out-of-Pocket (deductible, coinsurance, copay).

What are the benefits of an indemnity plan?

- Covering the remaining expenses (deductible, copay, co-insurance) that you might have with your primary plan on routine exams, hospitalization, surgery, medications, etc…

- Compensating for the possible loss of your income in case of accident or illness.

Indemnity plan & health insurance: different limits.

- With a traditional health plan, although the daily and annual limits of your plan represent thousands or even millions of dollars, you remain responsible for the payment of your deductible, co-payment, co-insurance etc…

- With an indemnity plan, the amount offered is usually only a few hundred or a few thousand dollars depending on the medical care received to help you pay your remaining expenses. Therefore, an indemnity plan is insufficient to completely cover you.

The network

With an indemnity plan, you do not have to respect a network of doctors to receive your benefits. However, remember that in your network, rates are often negotiated, and your remaining expenses are therefore lower.

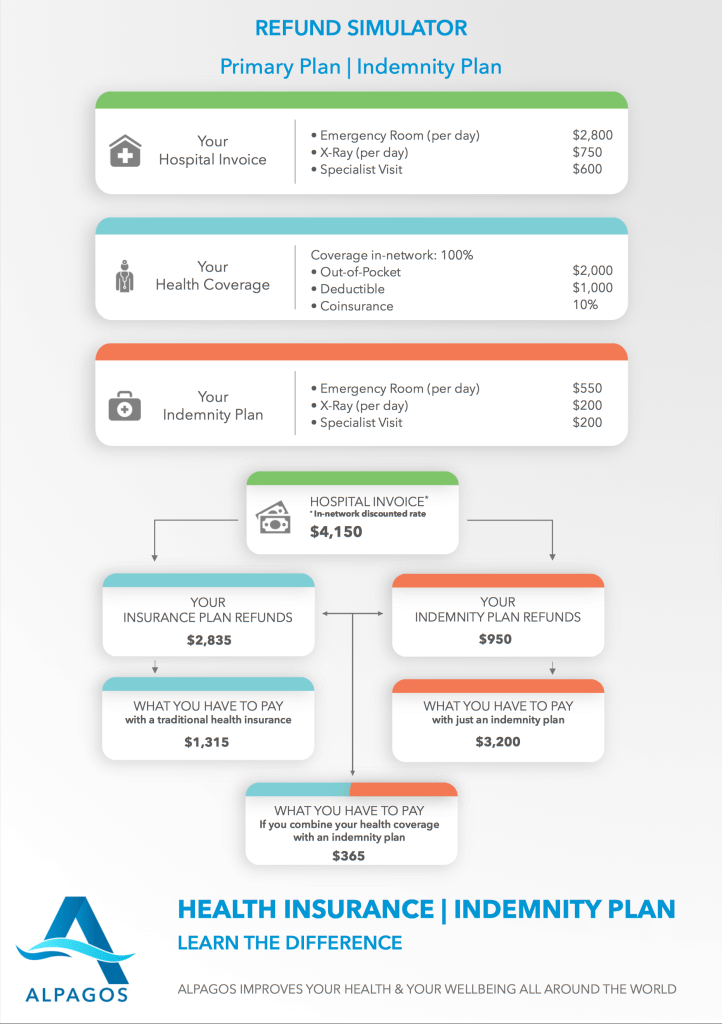

Refund Simulator, how does it concretely work?

“Let’s say, you are working out at home and you broke 2 of your fingers by accident. You go to the Emergency Room, you need an X-Ray and a specialist visit to be sure you are fine.”